Deep Dive into DuPont

Not as special as you might think.

I’ve had a lot of people ask me to do a deep dive on a public chemical company and I’ve resisted for a multitude of reasons, but I think it’s because I have no idea how to approach it. I’m not a public markets analyst. I do not want to pretend to be a public market analyst—I wouldn’t even know how to pretend. This is not investment advice. This is just some opinions. I’ll try to provide citations as I go via hyperlinks.

DuPont is a commoditized specialty chemicals business masquerading as a “true” specialty business through the acquisition of the Laird electronics business. The company is still eating the innovations from the 1950-1970s (maybe some of the 80s), but it’s just a bit more downstream in the product process. Instead of making their money through just making synthetic polymers an outsized amount of their revenue comes from converting commodity plastic or commoditized specialty polymers into end products. We can think of end products as things like Tyvek—the most basic of building wraps made from polyethylene and in the building products world is considered a commodity. Filtration membranes are another example where the raw materials might be associated with ion exchange resins or polyamides (commoditized resins), but DuPont sells the “finished” product to the end users. Instead of viewing the company as a true chemicals company they are closer to a Berry Global, Saint-Gobain, or Pall Corporation. The difference here is that DuPont is less focused that those aforementioned comparisons. I think there is more turmoil ahead for DuPont, especially if you were to dive into their numbers.

DuPont - The Original Specialty Pivot

The DuPont that we know from today started in 1920, but for the first 120 years of the company’s history they sold tools of death. From about 1802-1920 DuPont de Nemours, Inc (DuPont) focused on selling energetic materials: gunpowder, nitrocellulose, nitroglycerin, and trinitrotoluene (TNT). In 1928, DuPont made a bet on hiring a chemist named Wallace Carothers (A Mount Rushmore of polymer chemists for many) and the company would then help invent commercialization of synthetic polymer chemistry with Bakelite and ICI.

Wallace Carothers and his team helped to prove the hypothesis that covalently bonded polymers actually existed during a time when many chemists thought they were just aggregations of molecules. Carothers started working in 1928 at DuPont’s Experimental Station and together with Arnold Collins, produce chloroprene and eventually neoprene. Carothers and Hill would produce polyesters, polyanhydrides, but their instability (e.g., would fall apart in hot water) prohibited their usefulness. Carothers would then team up with Peterson and Coffman to do fundamental research in polyamides making crystalline domains. After Carothers returned to work from Johns Hopkins due to severe depression he worked with Gerard Berchet and George Graves on polymerizing hexamethylene diamine with adipic acid to produce nylon 6-6 or PA-66 in 1935. Graves would eventually take over for Carothers on the nylon project and DuPont would commercialize Nylon in tooth brush bristles, stockings, and parachutes from 1938 to 1940. Carothers committed suicide in 1937 and DuPont’s materials science focused products took off shortly afterwards. The successful pivot of DuPont essentially hinged on one of the first polymer chemists struggling with severe depression conducting academic work in a private enterprise environment with an eventual goal of commercialization.

If this feels grim or sad then I would trust your instincts.

Flush with cash from the success of Nylon, DuPont would then go on to invest in polymer chemistry research, and that investment paid off big. From 1950-1970s they came out with hit products—some are common household names today:

Mylar and Dacron - Polyethylene terephthalate - PET both as fibers and sheets

Orlon - polyacrylic fibers

Lycra - polyether urea/urethane fibers

Tyvek - high density polyethylene fibers as a non-woven mat

Nomex - polyaramid fibers (meta-aramids for the nerds)

Qiana - specialty nylon based on 4,4’-diaminodicylcohexylmethane and dodecanoic acid

Corfam - polyurethane and the original “pleather” or fake leather

Corian - acrylic filled with alumina trihydrate (original synthetic stone countertop)

Kevlar - polyaramid (para-aramid, and used in body armor all over the world)

Teflon - polytetrafluoroethylene (PTFE and the original PFAS)

Delrin/Hostaform - polyacetal (polyformaldyhde), a nice low friction resin that machinists love to machine (Staudinger won a Nobel prize for his work in this polymer and polymer chemistry in general. I think if Carothers had survived he would have shared the Nobel prize with Staudinger.)

The amount of innovation here seems staggering, but over the years DuPont would eventually sell off parts of the business that it had developed and made household names. They would also start working in the agriculture space and competing against companies like Monsanto. A lot of the innovation work came from fundamental research at DuPont’s Experimental Station. Someone once told me a story (no way can I know if this is true—pure polymer chemistry gossip) about DuPont reaching its innovation peak when the greenhouses were filled with growing tulips so that a polymer chemist could harvest Tulipalin in order to see if they could polymerize it. In late 2015 early 2016 DuPont closed Experimental Station and it would embark on another transformational journey. To me, this marked the end of a central R&D model and represents the capitalists fully exerting their control (I suspect they always did have control). These were troubling years for DuPont for numerous reasons but consider the R&D model, that got them the business successes they are still subsisting on today, as dead.

Chemours Spinoff and Merger with Dow

The issue with Teflon is that it’s tricky to process. If you want to be able to scramble eggs and get them out of a pan without using any butter or have waterproof boots without using high oil leather and minimal stitching, then you are going to pay a price. That price turned out to be perfluorooctanoic acid or PFOA, a processing aid for polytetrafluoroethylene PTFE, or Teflon. Intentional improper disposal of PFOA and similar chemicals as non-regulated waste meant that this stuff could be dumped in a landfill and it made it’s way to ground water. It eventually got some cows sick and Rob Bilott took on a landmark environmental case. The rest is recent history and Mark Ruffalo starred in the movie Dark Waters. The lesson to learn here:

DO NOT DUMP CHEMICALS INTO A LANDFILL OR DOWN THE SINK.

Get that tattooed somewhere on your body if you have trouble forgetting it.

The lawsuits and liability for DuPont became so big due to this absolute fuck up that they spun the entire business of Teflon into a new company called Chemours. Many analysts believed that Chemours was just a way for DuPont to dump their “risk.” DuPont and Chemours later settled many of the cases, recently a $110 million dollar settlement for the state of Ohio (Ohio and the chemical industry have an abusive relationship) and more recently about $1.185 billion dollars to resolve all PFAS-related drinking water claims.

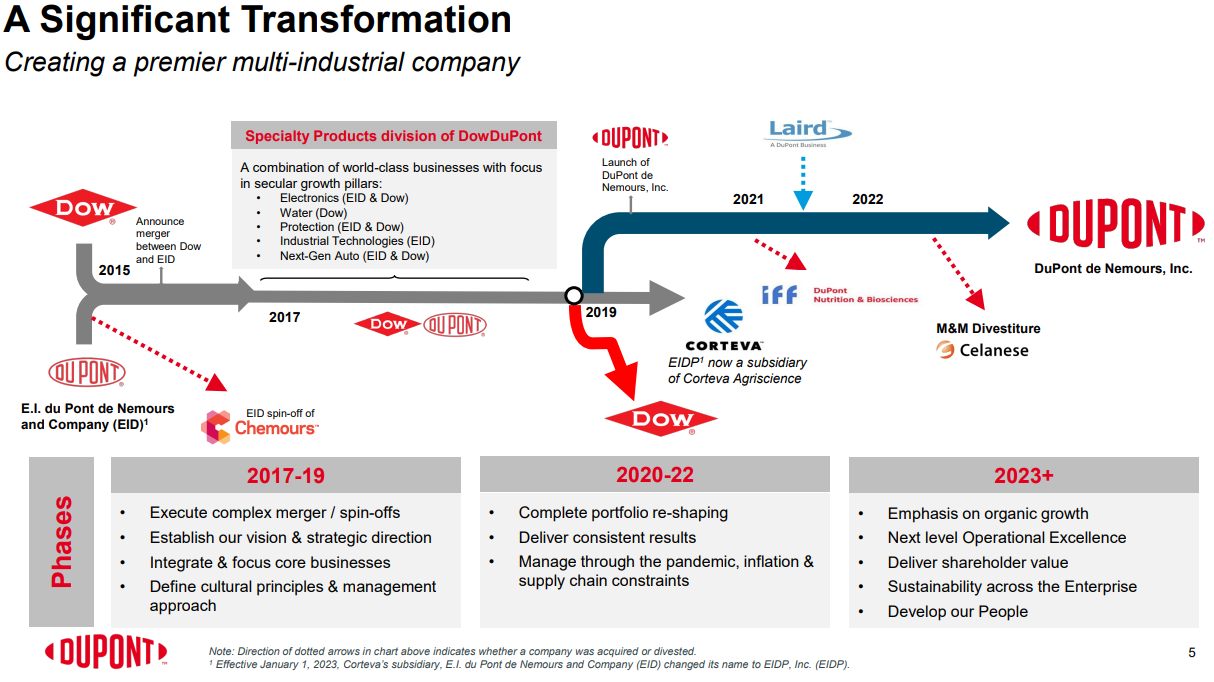

In Chemours issues wasn’t singular, in fact there was a bunch of probable risk on DuPont’s books from their agriculture division, and who knew what else. The only thing worse than declining profit margins in a chemical company is pairing that decline with an increased risk for litigation. Thus, the transformation of DuPont began by merging with Dow.

The ultimate plan with the Dow merger was to spin off the combined agriculture business (now known as Corteva) and for Dow to take the combined “commodity” businesses and for DuPont to take the “specialty” business. You can see their plan in the slide below from their investor deck:

By mid 2021 DuPont had spun off their biologics division to IFF, bought Laird, and divested the legacy Nylon business to Celanese. I wrote about this last year. The current DuPont is supposed to be a specialty powerhouse focused on five “pillars of excellence” or business units:

Electronics: Laird acquisition, some others, and existing parts of business like Kapton (polyimides) and conducting adhesives (epoxy resin)

Water Filtration: Ion exchange resins like Amberlite and nylon-based filtration membranes (FilmTec)

Protection: Tyvek, Styrofoam, DIY polyurethane foam, Kevlar, Nomex

Industrial Technologies: (silicone tubing, o-rings, antifriction coatings, Tedlar (polyvinyl fluoride)

Automotive: Formulated epoxy-based adhesives (formulated epoxy resins from when DOW had that business but spun off their base resins business as Olin), Nomex coatings, molykote coatings, electromagnetic interference shielding (carbon composites).

The only areas where a synthetic polymer chemist is needed would be in the electronics division and maybe a few working on aramids and antifriction coatings. The only reason to do synthesis is because there is probably some sort of high value opportunity out there that can pay back the R&D investment and my bet is electronics will be the best place to go if you are interested in synthetic polymer chemistry. The rest of DuPont is for polymer engineers who feel comfortable taking existing polymers and trying to convert them into something “special.”

Converting Polymers into Products

The more I think about it and dig at what is truly behind each “pillar” is just all of the old polymer chemistry from the 1950-1970s being converted or packaged a bit differently.

Within a supply chain we can think of going from the most raw of raw materials like petroleum and those raw materials being refined and converted into products that someone else turns into another product. For example, an oil company might refine some crude oil. Someone else might refine it to butane. Someone cracks it into butadiene. Maybe someone else hits it with hydrogen cyanide and hydrogenates to hexamethylene diamine. Someone takes that diamine and reacts it with adipic acid to make nylon 6,6 and then someone converts that nylon into a water filtration membrane.

DuPont used to be in the business of making the Nylon. They are still in that sort of business a bit with the acquisition of Laird in terms of electronics resins and the Kevlar business, but a huge amount of their revenue comes from just converting resins like nylon or polyethylene into the product that someone might put in your house. This is less “chemical company,” and more industrial products producer like Saint-Gobain or Pall Corporation. Traditionally, the further down the supply chain you move the higher the gross margins should be on your products, but you also have higher risk of finished goods getting scrapped. A bad batch of nylon or polyethylene could probably be worked off by mixing it with good resins or selling it at a steep discount, but a bad set of filtration membranes or 10,000 yard jumbo rolls of non-wovens is a harder sell.

DuPont doesn’t make epoxy resins, but they buy base resins and formulate them into adhesives for companies like Ford or Tesla.

DuPont doesn’t necessarily make the resins that go into Corian, they make the actual countertops with all of the effects and sell it to Home Depot so someone in an orange apron can upsell you from a basic laminated paper countertop to Corian, “look, we can do a waterfall effect in your kitchen island and it’s going to look just like quartz, but for less money!” Just don’t put anything really hot on there because it’s just acrylic with some aluminum trihydrate afterall.

DuPont is just a converter, maybe with a bit of vertical integration, but I think very little of their original chemical company DNA exists today.

By the Numbers

The DuPont specialty transformation looks good at first glance, but there is nothing that special here except for the electronics business. In reality, it’s some cash cows such as Tyvek, Nomex, Kevlar, Styrofoam, Epoxy resin adhesives, Amberlite, Kapton, and Tedlar that need minimal innovation support next to a true specialty electronics chemical company (Laird acquisition). I suspect some group at McKinsey (or BCG or Bain) was paid millions of dollars to get this whole thing into place. I just don’t think it’s played out exactly how it was supposed to go just yet.

For fiscal year of 2023 DuPont reported the following highlights:

$12.1 billion in net sales (-7% versus prior year)

Operating EBITDA Non-GAAP* (GAAP = Generally accepted accounting practice) $2.9 billion

This implies ~24% EBITDA margin, but non-GAAP. If non-GAAP sounds familiar it’s associated with the downfall of Enron.

Adjusted free cash flow* $1.6 billion

*Feels a bit suspicious to me and reads like a WeWork earnings report of community EBITDA

I couldn’t find the GAAP numbers for 2023, but in FY 2022:

$13.0 billion in revenue (slide 10 of 49)

$1.448 billion in earnings before incomes taxes (slide 48)

Roughly 11% EBITDA? I’m not an accountant though so all you finance nerds can check me on this. Also, no big settlement in 2022.

Essentially, from what I can tell (and I’m not an accountant or finance person) is that DuPont is struggling to get profits commiserate with a true specialty chemical company and they are more akin to a commodities company. This could be due to a few things that I’ve highlighted below in their FY 2023 report:

The various settlements the company was involved in appeared to cost $804 million (presumably not going to happen in 2024 and an increase from 2022).

Selling, General, and Administrative Expenses (SG&A) cost about $1.4 billion (yearly) or 11% of revenue (decline from 2022, this is good).

Debt costs were around $396 million (decline from 2022, this is good too).

R&D was at $508 million, or 4% of revenue (decline from 2022, depends on how you look at it, but probably not great).

Overall, I’m a bit disappointed that the company is not able to return higher profits to shareholders. I guess it’s a competitive market out there. I think the main issue here is that the true specialty division (electronics) is getting held back by the other cash cows. This feels ripe for an activist investor like Starboard to come in and shake things up (they already messed with DuPont on the Rogers acquisition and Corteva).

This is my first time digging into a public company. I have no stock in the company. I’m not shorting it. Just mostly for entertainment and my own curiosity. Let me know how I did or if you have a different take on the company in the comments.

Overall love the history, great for product knowledge. The finance info is okay and I suspect you’re going to get wicked good after doing other companies.

Interested on if chemours is liable. Does that mean DuPont as the original maker would also be liable as well? Obv I’m not a lawyer but I’m not sure about precedent yet for transferring liability.

My understanding is that there are environmental liabilities all over the place with all the bits and pieces that were once DuPont -- PFAS is only part of the story (a big part, though).